.png)

Key Takeaways

- Credit Risk Analysis Evolution: Traditional manual credit analysis taking 5-10 days replaced by AI-driven credit risk assessment delivering decisions in minutes, with ML models achieving 0.80-0.90 ROC AUC vs. 0.65-0.75 for traditional scores

- Real-Time Credit Risk Analytics: 50ms processing enables continuous credit portfolio risk monitoring vs. delayed quarterly credit risk reporting cycles

- Alternative Data Integration: Digital credit risk management solutions incorporate utility payments, e-commerce patterns, and behavioral biometrics for underbanked population assessment

- Operational Efficiency: Credit risk management tools reduce false declines by 20-30%, automate regulatory compliance (Basel III, IFRS 9), and process thousands of concurrent applications

- Industry Transformation: Banks, fintechs, and e-commerce are implementing AI-powered credit risk management solutions for instant approvals, BNPL scoring, and fraud prevention

- Implementation Strategy: Successful digital credit analysis transformation requires phased deployment, API-first architecture, ML training, and robust governance frameworks

- Future Technologies: Quantum computing, blockchain verification, and climate risk assessment will revolutionize next-generation credit risk analytics platforms

Global financial institutions reported over $1.1 trillion in credit losses during 2020-2022, according to McKinsey's Global Banking Annual Review, driving lenders to embrace digital credit risk analysis solutions. Traditional methods—manual underwriting, financial-statement review, and credit bureau scores—no longer suffice against evolving threats and competitive pressures. Digital and AI-driven approaches utilize real-time data, machine learning, and alternative data sources to expedite decision-making, enhance accuracy, and expand financial inclusion.

This trend overview examines the transformation from traditional credit analysis to AI-driven approaches, comparing methodologies, exploring industry applications, and providing implementation strategies for modernizing credit risk frameworks.

What Is Credit Risk Analysis?

Credit risk analysis evaluates the probability that a borrower will default on loan obligations. This systematic assessment forms the foundation of sound lending decisions and effective portfolio management.

Fundamental Components of Credit Risk Modeling

Credit risk modeling primarily involves quantifying three key metrics:

- Probability of Default (PD)

- Exposure at Default (EAD)

- Loss Given Default (LGD)

Beyond these core quantifiable metrics, effective credit risk management also incorporates critical elements such as:

- Risk Modeling & Stress Testing: This involves building models to assess portfolio resilience and conducting simulations to evaluate performance under various adverse economic scenarios, crucial for regulatory compliance and strategic planning.

- Underwriting & Decisioning: This refers to the application of credit risk models and data to automate and streamline the loan approval process, enabling efficient, real-time decisions that replace traditional manual underwriting.

Importance of Effective Credit Risk Management

Effective credit risk management significantly reduces loan losses, protects balance sheets, and ensures compliance with critical regulatory standards such as Basel III capital requirements and IFRS 9 expected credit loss provisions. By adopting robust risk frameworks, lenders can optimize capital allocation, better manage economic cycles, and support sustainable growth while potentially expanding access to credit for underserved populations.

Learn more about What is Credit Risk Assessment? A Beginner's Guide

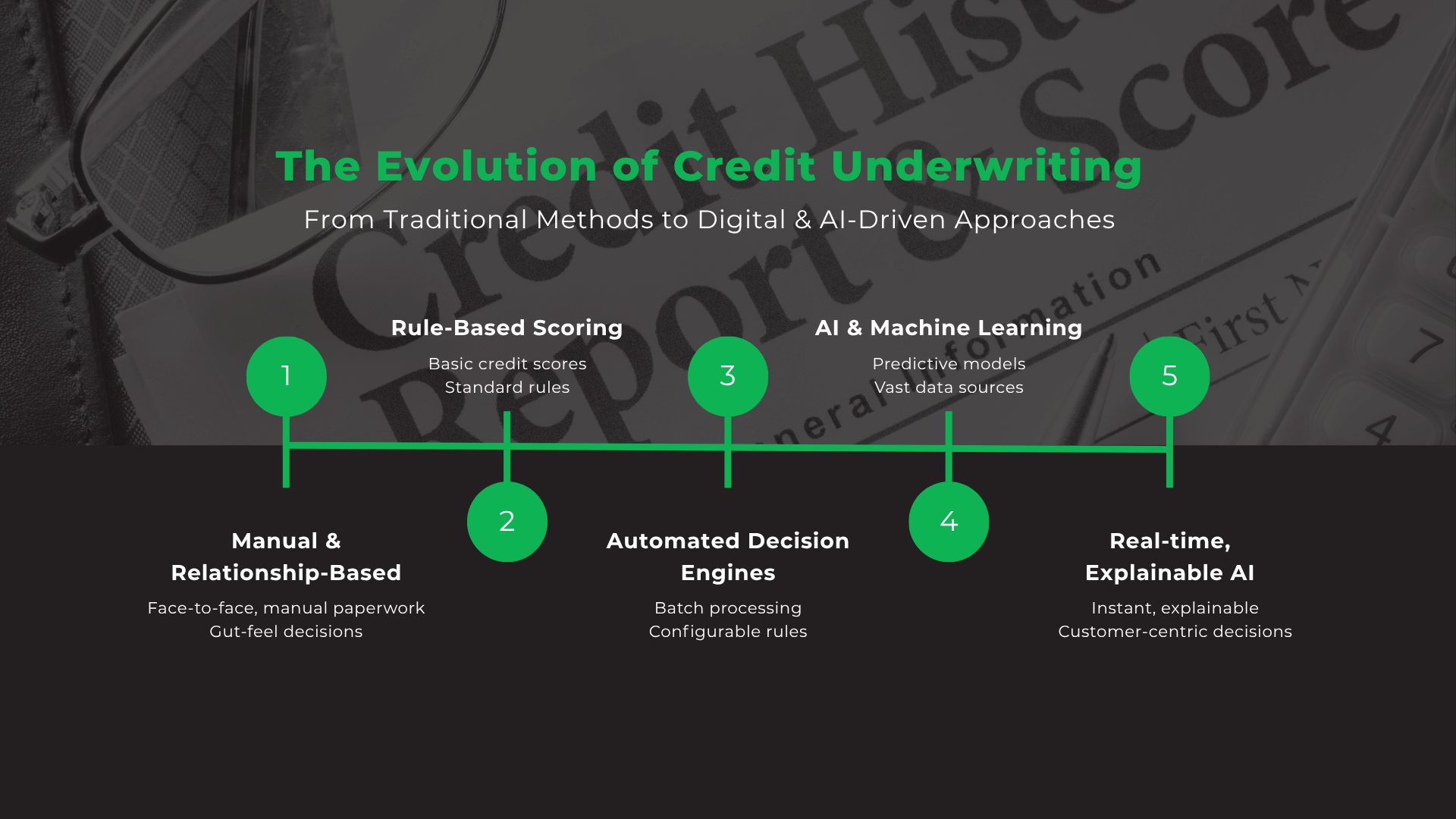

Traditional Credit Risk Analysis: Foundations & Limitations

How Did Banks Use Manual Underwriting to Assess Credit Risk?

- Financial Statement Analysis: Ratio analysis examined debt-to-equity ratios, current ratios, and cash-flow forecasting to evaluate borrowers' financial health. Underwriters spent hours reviewing tax returns, bank statements, and profit-and-loss statements.

- Credit Bureau Scores: Standardized scores based on payment history, credit utilization, length of credit history, new credit inquiries, and account types provide consistent risk assessment across borrowers.

- Collateral-Based Lending: Secured loans leveraged real estate, equipment, or inventory as collateral to mitigate default risk, requiring detailed appraisals and legal documentation.

These methods required extensive documentation, site visits, and underwriter expertise. While they provided clear creditworthiness views for established borrowers, the process was time-consuming and often excluded thin-file or underbanked customers.

What Are the Drawbacks of Traditional Credit Scoring & Analysis?

- Time-Intensive Underwriting: Manual processes—from document collection to committee reviews—took days or weeks, creating poor customer experiences and lost business opportunities.

- Limited Data Coverage: Reliance on credit bureau data and financial statements ignored alternative signals such as digital footprints, utility payments, and e-commerce activity that could indicate creditworthiness.

- Inconsistent Decisioning: Human bias and departmental silos led to variations in risk appetite and pricing, creating compliance challenges and unfair lending practices.

- Thin-File Borrower Exclusion: New-to-credit or underbanked individuals lacked sufficient credit history, resulting in loan denials or high interest rates despite actual creditworthiness.

Why Static Credit Risk Reporting Falls Short

Traditional reporting delivered delayed insights through monthly or quarterly cycles, hindering timely portfolio adjustments. Fragmented data sources across disconnected spreadsheets and legacy systems hindered holistic views of borrower behavior.

Without real-time visibility, lenders cannot detect emerging risks, such as sudden changes in payment patterns, which expose them to unexpected defaults.

Digital Credit Risk Management: Technologies & Best Practices

How Has Real-Time Data Processing Revolutionized Credit Risk Assessment?

- Streaming Analytics: Technologies like Apache Kafka and Spark enable ingestion of transaction streams, payment histories, and third-party feeds with 50ms latency, providing instant risk insights.

- Automated Decision Workflows: Rules engines and ML pipelines execute underwriting decisions instantly, reducing approval times from days to minutes while maintaining risk standards.

- API-First Architecture: Seamless integration with core banking systems, CRM platforms, and external data providers ensures flexibility and scalability for evolving business needs.

Real-time processing gives lenders up-to-the-second insights into borrower behavior, market shifts, and portfolio-level risk exposures, enabling proactive risk management.

Role of Alternative Data in Credit Risk Analysis

- Social Media & Digital Footprints: Public social signals including job history and network connections augment traditional credit profiles, especially valuable for thin-file borrowers.

- Utility & Telecom Payment Histories: Regular payment of phone, electricity, or rent bills provides additional proof of financial responsibility beyond traditional credit accounts.

- E-Commerce & Mobile Transaction Patterns: Purchase frequency, basket size, and merchant categories reveal spending behavior and potential default risk indicators.

Alternative data broadens credit access by incorporating behavioral and non-financial signals, enhancing predictive accuracy for new-to-credit segments while maintaining responsible lending standards.

Learn more about What is Alternative Data & How it Helps with Financial Inclusion

How Do ML & Behavioral Analytics Boost Credit Risk Accuracy?

- Supervised Learning Models: Logistic regression, XGBoost, and random forest algorithms trained on labeled datasets predict default probabilities with precision, often achieving ROC AUC scores above 0.80.

- Unsupervised Anomaly Detection: Clustering and autoencoder algorithms identify outliers like unusual transaction spikes or synthetic identities without requiring pre-labeled examples.

- Behavioral Scoring: Monitors clickstream data, mobile app usage, and device fingerprints to detect deviations from established borrower profiles.

- Cross-Channel Correlation: Combines online, branch, and call-center interactions to create 360-degree customer views, revealing hidden risk patterns overlooked by single-channel systems.

AI-Driven Credit Risk Analytics: Models & Applications

Which Machine Learning Models Predict Credit Default Most Accurately?

- Decision Trees & Ensemble Methods: Random forests and gradient boosting machines like XGBoost and LightGBM excel at handling non-linear relationships and feature interactions, achieving high predictive power.

- Neural Networks & Deep Learning: Multi-layer perceptrons and recurrent architectures capture complex patterns in time-series data and learn hierarchical feature representations from payment histories.

- Unsupervised Learning Models: K-means clustering and DBSCAN detect novel fraud schemes and segment borrowers into risk categories without labeled data.

These models enable credit risk teams to build robust scoring pipelines that adapt to changing market dynamics and emerging fraud patterns.

How Does Real-Time Portfolio Risk Monitoring Work in Digital Banking?

- Continuous Risk Scoring: Streaming risk engines score each borrower in real-time, updating risk metrics as new data arrives to immediately identify deteriorating risk.

- Dynamic Portfolio Rebalancing: Automated rules adjust portfolio allocations, reducing exposure to high-risk segments and reallocating capital based on real-time dashboards.

- Early Warning Systems: Threshold-based alerts notify risk officers of sudden spikes in delinquencies, concentration risk, or adverse macroeconomic indicators.

- Automated Stress Testing: Simulations evaluate portfolio resilience under predefined scenarios in minutes rather than weeks, informing capital planning and provisioning.

Top Benefits of Automated Credit Risk Analytics for Lenders

- Accelerated Processing: Underwriting decisions shift from days to minutes, accelerating loan origination and improving customer satisfaction while reducing operational costs.

- Consistent Decision-Making: Automated models apply uniform criteria across all applications, minimizing human biases and ensuring regulatory compliance.

- Enhanced Fraud Detection: Behavioral analytics and device fingerprints identify application fraud or identity theft before loan disbursement, protecting lenders from losses.

- Improved Compliance: Automated reporting for Basel III, IFRS 9, and data privacy regulations reduces audit risk and operational overhead.

Traditional vs. Digital Credit Risk Management: Key Comparisons

Speed & Efficiency: Digital vs. Manual Underwriting

- Traditional Underwriting: 5-10 business days from application to decision, requiring document verification, manual committee reviews, and paper-based processes.

- Digital Methods: Minutes to hours with automated data ingestion, ML scoring, and e-signature workflows enabling same-day or instant approvals.

- Processing Volume: Digital platforms handle thousands of applications concurrently at a fraction of operational cost per loan, while manual processes scale linearly with headcount.

Accuracy & Precision: ML-Based Scoring vs. Traditional Models

- Default Prediction: ML models often achieve ROC AUC of 0.80-0.90, compared to 0.65-0.75 for traditional credit bureau scores.

- False Positive Reduction: Behavioral signals and alternative data reduce false declines by 20-30%, improving customer acquisition while maintaining low default rates.

- Risk-Adjusted Pricing: Granular risk scores enable personalized interest rates, boosting yield on low-risk borrowers while mitigating high-risk exposure.

Data Coverage: 360° Customer View vs. Credit Bureau Data

- Traditional Sources: Credit bureaus, audited financial statements, and collateral details—often delayed or incomplete for new-to-credit borrowers.

- Digital Data Spectrum: Alternative data including utility payments and e-commerce transactions, behavioral insights from digital footprints, and real-time third-party risk feeds.

- Inclusion Benefits: Leveraging non-traditional data enables assessment of gig-economy workers, immigrants, and students, expanding financial inclusion responsibly.

Industry Use Cases: Credit Risk Solutions in Banking, Fintech & E-Commerce

How Do Banks Use AI for Retail & Commercial Credit Risk?

- Retail Lending Automation: Real-time scoring engines ingest salary data, transaction histories, and digital footprints to instantly approve consumer loans while ensuring AML compliance.

- Commercial Credit Assessment: Automated analysis of corporate financials, cash-flow projections, and supplier data provides rapid credit lines to SMEs through ML models.

- Portfolio Management: Real-time dashboards track delinquency trends and concentration risk, enabling data-driven credit limit adjustments.

Which Fintech Innovations Improve Digital Lending Risk Assessment?

- Instant Loan Engines: Visual underwriting workflows ingest mobile device data and eKYC results to approve microloans in minutes.

- P2P Lending Platforms: Utilize social trust scores and crowd-sourced risk assessments for dynamic loan pricing.

- BNPL Risk Scoring: Real-time ML models analyze purchase behavior and merchant data to underwrite transactions at checkout.

- Microfinance Applications: Leverage mobile-money records in emerging markets to build credit scores for unbanked populations.

How Do E-Commerce Platforms Integrate Credit Risk Management & Fraud Prevention?

- Seller Financing: ML models combine sales history, return rates, and customer feedback to finance high-volume merchants.

- Consumer Credit: Embedded payment options underwritten by real-time engines analyzing spending patterns.

- Cross-Border Analysis: Risk models incorporate geolocation and currency volatility for international transactions.

- Fraud Prevention: Behavioral scoring and velocity rules block suspicious orders before checkout completion.

How to Implement a Digital Credit Risk Management Framework

Transitioning from Traditional to Digital Credit Risk Analysis

- Phased Implementation: Start with high-impact products like personal loans to validate ML models and data integrations before scaling across additional products.

- Legacy Integration: Consolidate siloed data into centralized data lakes with ETL pipelines while building API layers for real-time connectivity.

- Change Management: Upskill teams on ML fundamentals and establish cross-functional governance committees for model validation and compliance.

Which Credit Risk Management Tools Should You Prioritize?

- Real-Time Scoring Engine: 50ms inference supporting thousands of events per second for instant decisioning.

- Alternative Data Connectors: APIs for utility, telecom, and e-commerce data to broaden credit coverage.

- ML Model Library: Pre-trained models for default prediction and anomaly detection with custom model support.

- Compliance Automation: Templates for Basel III, IFRS 9, and privacy regulations with audit trails.

- Scalable Architecture: Kubernetes-based microservices for horizontal scaling across cloud platforms.

How to Measure Success: KPIs & ROI in Credit Risk Analytics?

- Speed Metrics: Application-to-decision time improvement from days to minutes.

- Risk Metrics: NPL ratios and charge-off rates compared pre- and post-implementation.

- Accuracy Metrics: False positive/negative rates and risk-adjusted returns.

- Experience Metrics: Customer satisfaction scores and approval rates.

- Efficiency Metrics: Operational cost reduction and processing automation levels.

Conclusion: Why Credit Risk Analysis Is a Competitive Advantage

Digital credit risk analysis represents a strategic differentiator in today's competitive financial landscape. By harnessing real-time processing, alternative data, and advanced ML models, lenders transition from reactive reviews to proactive risk management—reducing losses, expanding access, and achieving faster decision cycles.

Success Factors:

- Robust governance and continuous model validation

- Comprehensive staff training and change management

- Investment in emerging technologies like quantum computing and collaborative intelligence

Financial institutions that adopt comprehensive digital strategies will be able to approve applications in minutes while maintaining low default rates, expand lending to underbanked populations, and meet regulatory requirements through automated reporting.

Ready to transform your credit risk framework? Contact TrustDecision to learn how our AI-driven platform can reduce defaults, accelerate approvals, and drive sustainable business growth.