%2520(1).png)

Key Points

- Alternative data enables credit assessment for 1.7 billion unbanked adults globally and millions more underbanked consumers through non-traditional signals like utility payments and mobile usage

- Financial institutions using alternative data see 40-point credit score improvements and 1.7% NPL rates in emerging markets

- Rent and utility payment history can build credit profiles for thin-file borrowers within 12 months

- Privacy compliance (GDPR/CCPA) and bias testing are essential for responsible alternative data implementation

- Open banking and AI-powered behavioral modeling represent the future of inclusive credit assessment

Introduction: The Financial Inclusion Crisis and Alternative Data Solution

Nearly 1.7 billion adults worldwide remain unbanked, while 1.1 billion of them own a mobile phone but lack access to comprehensive financial services. Traditional credit scoring creates a fundamental catch-22: consumers need credit history to access financial services, but cannot build that history without initial access.

Alternative data in finance, consisting of non-traditional financial information such as mobile payments, utility usage, and device metadata, is revolutionizing credit assessment by enabling lenders to evaluate creditworthiness beyond bureau scores. In Southeast Asia alone, where 70% of the population remains unbanked or underbanked, this represents a $250+ billion market opportunity.

The business case is compelling: Financial institutions using alternative data achieve significantly lower non-performing loan rates and substantial credit score improvements within 12 months, enabling profitable expansion to previously inaccessible segments while maintaining responsible risk management.

Understanding Alternative Data

What Is Alternative Data in Credit Assessment?

Alternative data in credit assessment refers to non-traditional information sources that supplement or replace conventional credit bureau data to evaluate borrower creditworthiness. This includes behavioral patterns, payment histories, and digital activities that demonstrate financial responsibility outside formal credit relationships.

Alternative Credit Scoring Data Sources

Types of alternative data encompass metrics outside traditional credit bureau information:

- Bank account behavior - Balance patterns, transaction consistency, and cash flow stability

- Utility & rent payments - Reliable payment signals for creditworthiness assessment

- Telecom usage & mobile metadata - Voice/text frequency, call-detail networks, and payment consistency

- Online activity & device data - Digital footprint consistency, device fingerprints, and app usage patterns

- Public records - Employment history, professional licenses, and legal filings (excluding bankruptcy where restricted)

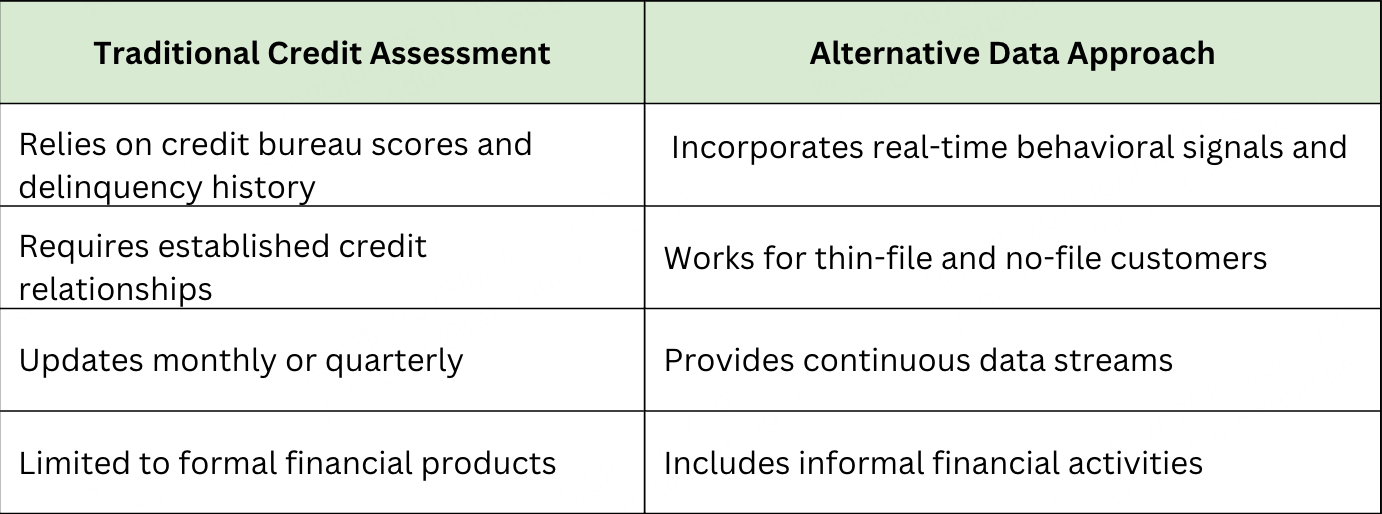

What is the Difference Between Alternative Data vs Traditional Credit Data?

While traditional credit assessment relies on historical bureau data, alternative data provides real-time behavioral insights that work for customers with limited credit histories.

This fundamental difference enables lenders to broaden credit assessment capabilities while maintaining robust risk discipline. With this foundation established, let's examine how alternative data drives financial inclusion in practice.

How Alternative Data Drives Financial Inclusion

Alternative data is revolutionizing financial inclusion by enabling lenders to accurately assess the creditworthiness of historically excluded populations. This innovative approach profiles previously "invisible" individuals, expanding access to essential financial services and fostering economic empowerment.

How Does Alternative Data Improve Credit Access for the Unbanked?

By analyzing real-world payment behaviors and digital patterns that traditional credit files miss, alternative data allows financial institutions to safely extend credit to thin-file and no-file borrowers, including young adults, immigrants, and gig workers.

Target Populations Benefiting:

- Young adults (18-25) with limited credit history but strong digital payment patterns

- Gig economy workers with irregular income but consistent utility/rent payments

- Recent immigrants lacking credit history but demonstrating financial responsibility

- Underbanked consumers using alternative financial services but excluded from traditional credit

What Alternative Data Sources Can Lenders Use for Credit Assessment?

- Mobile money transaction patterns and consistency

- Utility payment reliability and amount stability

- Digital service subscriptions and payment behavior

- Employment verification through payroll data

Leveraging these diverse data sources, the effectiveness of alternative data in credit assessment is clearly demonstrated through quantifiable success metrics.

What Are the Proven Benefits of Using Alternative Data?

The real power of alternative data lies in its measurable results. Here are key metrics demonstrating how it improves credit scores, enhances risk management, and drives financial gains for lenders:

Credit Access Improvements:

- 40-point average credit score gains over 12 months through payment history reporting

- 10-15% increase in loan approval rates for thin-file customers

- 25-30% reduction in manual underwriting costs through automation

Risk Management Benefits:

- 1.7% NPL rates achieved by comprehensive alternative data users (vs 3-5% industry average)

- 20% improvement in default prediction accuracy with combined data signals

- 50% reduction in fraud rates through device fingerprinting and behavioral analysis

Why Alternative Data Is a Strategic Advantage

Combining traditional and alternative signals creates comprehensive credit profiles that:

- Lower risk premiums for previously underserved segments

- Expand the addressable market beyond traditional credit bureau coverage

- Enable responsible lending through better risk assessment

- Improve customer lifetime value through earlier relationship building

Business Impact: How Alternative Data in Financial Services Transforms Operations

Implementing alternative data in credit assessment offers profound advantages, transforming how financial institutions operate and grow. It's a strategic shift that not only mitigates risk but also unlocks significant market opportunities.

Strategic Benefits of Alternative Data for Finance

Alternative data fosters both business growth and market differentiation:

Market Expansion and Revenue Growth:

- Expands credit access - Reaches populations not served by traditional bureau-based models

- Enhances risk precision - Enables real-time risk scoring and adaptive decision-making

- Supports customer acquisition - Builds relationships with emerging consumer segments

- Improves competitive positioning - Differentiates services through inclusive lending capabilities

Operational Efficiency and Risk Management:

- Fraud resistance - Device and behavioral inconsistencies signal potential fraud

- Reduced lending costs - Digital, automated analytics drive operational efficiency

- Portfolio diversification - Access to new customer segments reduces concentration risk

- Regulatory alignment - Supports fair lending and financial inclusion mandates

Alternative data, therefore, is not just an enhancement but a powerful catalyst for growth, efficiency, and compliance in financial services. While the benefits are compelling, successful implementation requires addressing specific challenges.

Implementation Challenges and Solutions

Successfully integrating alternative data into credit assessment presents inherent challenges. Overcoming these hurdles requires a strategic approach focused on compliance, data integrity, and technical adaptability, which is crucial for maximizing its benefits and ensuring responsible deployment.

What Are the Challenges with Alternative Data?

Privacy and Regulatory Compliance

Challenge: User consent and privacy protection requirements

Solutions:

- Explicit consent frameworks compliant with CCPA and GDPR.

- Data minimization strategies that collect only necessary information.

- Transparent data usage policies and customer communication.

Data Quality and Bias Management

Challenge: Inaccuracies from telecom or public data sources and potential discrimination

Solutions:

- Multi-source data validation and cross-verification processes.

- Algorithmic bias testing across demographic groups.

- Regular model performance monitoring and adjustment.

- Fairness testing aligned with FCRA and ECOA requirements.

What Are the Key Technical Requirements for Alternative Data Implementation?

Essential requirements include API-first integration architectures, real-time data processing capabilities, comprehensive data governance frameworks with automated validation, scalable cloud infrastructure, and advanced analytics platforms supporting machine learning deployment. Organizations also need data scientists experienced in alternative credit modeling, compliance specialists, and technical teams for maintaining complex data pipelines.

Technical Integration and Explainability

Challenge: System integration and model transparency requirements

Solutions:

- API-first integration architectures for gradual implementation.

- Explainable AI tools (SHAP/LIME) for decision transparency.

- Comprehensive documentation and audit trails for regulatory compliance.

Alternative Data in Action: Global Case Studies

Real-world implementations demonstrate how alternative data successfully expands financial inclusion across diverse markets and customer segments. These case studies showcase practical approaches to alternative data integration, quantifiable business results, and key success factors that enable sustainable lending to previously underserved populations.

Emerging Market Innovation: Verqor in Mexico

- Implementation: Leverages five years of trading data to assess smallholder farmer creditworthiness

- Results: Achieved 1.7% low non-performing loan rates through comprehensive behavioral analysis

- Key Success Factors: Deep domain expertise, localized data sources, community-based verification

Source: Financial Times. October 14, 2024. Lenders get creative to finance small businesses in developing markets

Mobile-First Approach: M-Kopa in Africa

- Implementation: Uses daily mobile money payments to build credit scores incrementally

- Scale: Reached over 5 million customers across Kenya, Uganda, and Ghana

- Innovation: Enables asset financing through micro-payment performance tracking

Source: Fintech Finance News. September 24, 2024. Leading Fintech M-KOPA Reaches 5 Million Customers, Unlocking $1.5Bn in Credit Across 5 Markets

Digital Ecosystem Innovation: Grab PayLater in Southeast Asia

- Implementation: Leverages transaction data from 25+ million monthly users across ride-hailing, food delivery, and payments to assess creditworthiness and offer customized BNPL limits

- Results: Achieved 2x+ usage growth in fashion and beauty categories, with 9 in 10 Southeast Asians lacking credit cards gaining access to interest-free installments

- Key Success Factors: Ecosystem-wide data integration, strict whitelisting approach unlike credit card-based competitors, proactive guardrails including in-app notifications and transaction halting for missed payments

Source: 2C2P. October 20, 2023. Payments Powerhouses: Driving Digital Payments in Southeast Asia

Workforce-Focused Credit Access: KarmaLife in India

- Implementation: Uses employment data, attendance patterns, and earnings history from 40+ partner companies to provide Earned Wage Access (EWA) and small-ticket credit to 2+ million gig workers

- Results: Achieved 50% boost in worker retention, 10% increase in productivity, and became India's largest EWA platform serving blue-collar workers traditionally excluded from formal credit

- Key Success Factors: Partnership-based distribution model, earnings-linked credit assessment, transparent fee structure with regulatory compliance through RBI-authorized NBFCs

Source: KarmaLife Blog. September 12, 2024. Scaling Financial Flexibility: How KarmaLife Became India's Largest EWA Platform

These case studies demonstrate that successful alternative data implementation requires local market expertise, regulatory compliance, and comprehensive data integration strategies.

Their achievements demonstrate that financial inclusion initiatives can be both socially impactful and commercially viable, creating sustainable business models that serve underserved communities while generating returns for investors and stakeholders.

Future of Alternative Data in Financial Inclusion

The alternative data landscape is rapidly evolving with emerging technologies and regulatory frameworks that will further enhance financial inclusion capabilities.

TrustDecision is at the forefront of these advances, delivering solutions that promise more accurate risk assessment, stronger consumer protections, and expanded access to credit for underserved populations worldwide.

Emerging Technologies and Data Sources

TrustDecision's platform integrates cutting-edge technologies to maximize alternative data effectiveness:

- Open banking integration - Real-time account data and income verification through secure API connections

- AI-powered behavioral modeling - Advanced NLP analysis of utility and subscription patterns with TrustDecision's proprietary algorithms

- Explainable AI tools - Built-in SHAP/LIME frameworks ensuring transparency and regulatory compliance

- IoT and device data - Smart device usage patterns and location-based insights via TrustDecision's Device Intelligence

- Blockchain verification - Immutable identity and payment history records with enhanced security protocols

Regulatory Evolution and Industry Standards

TrustDecision helps financial institutions navigate the evolving regulatory landscape while maximizing alternative data benefits:

- Enhanced fair lending guidelines for AI-driven decisions with automated compliance monitoring

- Standardized frameworks for alternative data validation through TrustDecision's governance tools

- Consumer protection requirements for data transparency with built-in disclosure mechanisms

- Industry best practices for bias testing and mitigation via continuous model monitoring

For strategic guidance on future-ready implementations that leverage these emerging capabilities, explore TrustDecision's Enterprise Solution Evaluation Framework and discover how our comprehensive platform positions your institution at the forefront of inclusive finance innovation.

Conclusion: Building Inclusive Financial Systems Through Alternative Data Innovation

Alternative data in finance is revolutionizing credit access by enabling safe, fair financial inclusion for previously underserved populations. For bankers, fintech leaders, and policymakers, incorporating these signals has become essential for competitive differentiation and market expansion.

The evidence demonstrates that responsible alternative data implementation delivers measurable benefits: improved risk assessment, expanded market reach, and enhanced operational efficiency while maintaining regulatory compliance and consumer protection.

Next steps: Assess your institution's data capabilities, regulatory requirements, and target market opportunities to develop a comprehensive alternative data strategy.

Explore TrustDecision’s Credit Decisioning Solutions:

- Application Fraud Detection for enhanced security

- Credit Data Insight for real-time portfolio analytics

- Credit Risk Decisioning for comprehensive alternative data integration

Ready to transform your credit decisioning capabilities? Contact our solutions experts today to schedule a consultation.