Key Takeaways

- Fraud detection in banking is no longer siloed: Banks must move beyond standalone tools toward unified, enterprise-wide fraud management across onboarding, transactions, and ongoing account activity.

- Fraud risk spans the full customer lifecycle: Effective controls must address threats from digital onboarding and application fraud through account takeover, P2P scams, and lending fraud.

- AI and machine learning are now foundational to fraud prevention: AI-driven fraud detection enables real-time analysis of transactional, behavioural, and identity signals at scale.

- Real-time fraud detection improves outcomes: Millisecond-level decisioning reduces fraud losses while maintaining a low-friction customer experience.

- Integrated decisioning drives operational efficiency: Connecting identity verification, application fraud detection, transaction monitoring, and credit risk reduces false positives and manual reviews.

- Enterprise orchestration enables scale: ARCHER® Risk Decisioning OS and ARGUS® Fraud Management Platform unify fraud strategy and execution across the banking lifecycle.

Why Is Fraud Detection in Banking Becoming More Challenging?

Strengthening a bank’s defenses today requires deploying AI-driven, multi-layered fraud detection tools in banking that can adapt as threats evolve.

According to the PwC Global Economic Crime and Fraud Survey 2024, 41% of financial services organizations experienced fraud in the past two years, with

In parallel, the APAC Digital Banking Fraud Trends Report 2023 found that scams accounted for 54% of reported bank fraud cases, while voice scams increased by over 200% year-on-year.

Against a backdrop of post-pandemic disruption and geopolitical instability, fraudsters increasingly exploit human-centric vulnerabilities—leveraging social engineering, impersonation, and remote access manipulation to bypass even mature cybersecurity controls.

This evolving threat landscape has made artificial intelligence fraud detection in banking, combined with machine learning, essential to modern fraud detection and prevention as banks prepare for increasingly sophisticated fraud risks through 2026 and beyond.

What Are the Most Common Types of Bank Fraud Today?

Banks face a wide range of fraud threats across onboarding, transactions, and account access. Effective fraud prevention requires visibility across the entire customer lifecycle. The most common types of bank fraud today include:

Card Fraud

Card fraud remains one of the most prevalent forms of banking fraud, involving the unauthorised use of credit, debit, prepaid, or gift cards. Common techniques include card skimming, card-not-present (CNP) fraud, and card cloning.

Global card fraud losses reached USD 34 billion in 2023 and are projected to exceed USD 43 billion by 2026.

Learn how banks detect and prevent credit card fraud using real-time analytics and AI-driven risk signals in Credit Card Fraud Detection System: A Comparative Approach

Check Fraud

Check fraud exploits paper or digital checks to illegally withdraw funds. Typical tactics include forged signatures, altered checks, and checks drawn from closed or fictitious accounts.

According to the 2025 AFP® Payments Fraud and Control Survey (reflecting 2024 data), 63% of organizations reported experiencing check fraud, making checks the most frequently targeted payment method despite declining usage.

Friendly Fraud (Chargeback Fraud)

Friendly fraud occurs when legitimate customers dispute valid transactions, often claiming they were unauthorised. While not driven by external attackers, it still creates significant financial losses, operational overhead, and chargeback management costs for banks and merchants.

New Account Fraud

New account fraud—often associated with synthetic identity fraud—occurs when criminals open accounts using stolen, fabricated, or blended identities. These accounts are later exploited for fraudulent transactions, mule activity, or credit abuse.

Related insight: Learn how synthetic identity fraud works—and how banks can detect it during digital onboarding using behavioral and identity signals.

Account Takeover (ATO)

Account takeover fraud occurs when attackers gain unauthorised access to existing customer accounts. Common attack vectors include:

- Phishing and credential harvesting

- Credential stuffing and brute-force attacks

- Social engineering and impersonation

- Malware, ransomware, or data breaches

- Call centre fraud, increasingly linked to organized scam operations across Southeast Asia

See real-world examples of account takeover attacks—and how businesses prevent them using layered, AI-driven controls.

Money Laundering

Money laundering involves concealing the origins of illicit funds by moving them through legitimate financial systems. It typically occurs in three stages:

- Placement: Introducing illegal funds into the financial system, often through structured or small transactions

- Layering: Conducting complex transfers or transactions to obscure the source of funds

- Integration: Reintroducing funds as seemingly legitimate assets, such as through businesses, real estate, or investments

Explore the three major steps of money laundering—and how banks can detect suspicious activity at each stage in: 3 Major Steps in Money Laundering: Techniques and Prevention Strategies

P2P Payment Fraud

The rapid adoption of peer-to-peer (P2P) payment platforms—such as PayPal, Venmo, Google Pay, Apple Pay, Zelle, and Alipay—has introduced new fraud risks. Fraudsters exploit weak identity controls, social engineering, and limited contextual data.

Losses from P2P payment fraud were estimated at USD 1.7 billion in 2022, representing a ~90% year-over-year increase, driven largely by scam-based fraud.

Application and Loan Fraud

Application fraud and loan fraud occur when individuals use stolen, manipulated, or synthetic identities to obtain credit or loans—often exploiting gaps in digital onboarding, underwriting, or verification processes before losses become visible.

Common fraud patterns include:

- Loan stacking: Submitting multiple loan or credit applications across institutions within a short timeframe

- Gradual credit abuse: Establishing trust through small, legitimate transactions before rapidly increasing borrowing

- Synthetic identity fraud: Combining real and fabricated data to create new identities that evade traditional checks

The risk has intensified with the growth of digital lending. Loan fraud now spans personal loans, payday lending, and mortgages, driven by widely available personal data and automated approval flows.

According to CoreLogic’s Mortgage Fraud Report, about one in every 123 mortgage applications showed potential fraud risk in Q2 2024, marking an 8.3% year-over-year increase.

These schemes are often amplified by dishonest intermediaries. In some cases, loan brokers deliberately falsify borrower information to push applications through underwriting—exposing lenders to significant financial and regulatory risk.

Learn more in The Bad Apples of Loan Brokers: How They Falsify Borrowers and Defraud Lenders.

How AI-Based Fraud Detection in Banking Work

AI-based fraud detection in banking combines machine learning, behavioral analytics, and real-time decisioning to identify suspicious activity across the entire customer lifecycle. Instead of relying on static rules, AI models continuously learn from new data, enabling banks to detect both known fraud patterns and emerging threats with greater accuracy and speed.

This approach allows fraud detection and prevention in the banking industry to scale across digital onboarding, transactions, lending, and ongoing account activity—without introducing unnecessary friction for legitimate customers.

Why Are AI and Machine Learning Critical for Modern Fraud Detection?

Traditional rule-based systems struggle to keep pace with modern fraud, where attacks are faster, more coordinated, and increasingly cross-channel. Fraud detection in banking using machine learning enables institutions to analyze large volumes of data in real time, uncover complex and non-linear fraud patterns, and adapt quickly as fraud tactics evolve.

Machine learning models also help reduce false positives by distinguishing genuinely risky behavior from normal customer activity—an essential capability for balancing fraud prevention with customer experience.

Data Ingestion and Feature Engineering

AI-driven fraud detection tools in banking collect and standardize data from multiple sources to create a unified view of risk, including:

- Customer profiles and historical account data

- Transaction histories across digital and physical channels

- Behavioral signals such as login patterns and interaction anomalies

- Device and location intelligence revealing contextual risk

Through feature engineering, this raw data is transformed into meaningful fraud indicators that models can interpret. This process requires deep domain expertise to ensure features reflect real-world fraud behavior rather than surface-level anomalies.

Machine Learning Model Development

Modern AI-based fraud detection in banking leverages multiple model types:

- Decision Trees for explainable, rule-aligned decisions

- Neural Networks for detecting complex, non-linear fraud patterns

- Ensemble Models combining multiple algorithms for higher accuracy

By combining supervised learning (known fraud patterns) and unsupervised learning (anomaly detection), AI-based fraud detection systems deliver adaptive, resilient protection—capable of identifying both established and previously unseen threats.

Key Advantages of AI-Driven Fraud Detection in Banking

Beyond detection accuracy, AI-driven fraud detection delivers measurable operational and customer experience benefits—particularly in high-volume, multi-channel banking environments.

Real-Time Fraud Monitoring and Faster Risk Response

Real-time fraud detection analyzes transactions within milliseconds using AI-driven risk scores derived from multiple signals, including:

- Transaction behaviour and spending patterns

- Device intelligence and session attributes

- Location inconsistencies and geolocation anomalies

- Historical customer and account activity

This enables banks to identify and respond to suspicious activity as it occurs—blocking, flagging, or stepping up verification in real time—while allowing legitimate transactions to proceed with minimal friction.

Enterprise Fraud Management and Operational Efficiency at Scale

Enterprise fraud management centralises digital onboarding, lending, transaction monitoring, and ongoing account surveillance within a single decision framework. Rather than relying on fragmented point solutions, banks adopt a unified orchestration approach that coordinates data, rules, models, and workflows in real time across channels.

Within this architecture, fraud management functions as an execution capability—applying fraud controls to live events and transactions. It monitors activity across channels, evaluates risk in real time, and supports investigation and response workflows, translating centrally defined strategies into consistent operational actions across the banking lifecycle.

This approach enables banks to:

- Improve operational efficiency by reducing manual reviews and duplicated processes

- Lower false positives through consistent, cross-channel risk scoring

- Tailor fraud strategies to specific products, geographies, and regulatory requirements

- Strengthen cross-channel visibility by linking identity, behavioural, and transaction signals

By consolidating fraud decisions within a unified framework, banks reduce operational complexity while scaling fraud prevention more accurately and consistently.

However, efficiency gains depend not only on advanced analytics, but on how effectively fraud strategies are executed. Modern fraud programmes require a decisioning layer that applies controls uniformly and in real time across the entire banking lifecycle—bridging strategy and execution at enterprise scale.

Moving From Fraud Strategy to Execution

While AI and machine learning underpin modern fraud detection, their effectiveness depends on how seamlessly they are embedded into day-to-day operations. Banks must move beyond isolated tools and adopt a unified approach that connects identity verification, application fraud detection, transaction monitoring, and credit risk decisioning in real time.

To operationalise this model, banks need an enterprise-grade platform that can centrally govern fraud strategy while executing fraud controls in real time across channels—without reintroducing silos or operational friction.

How TrustDecision Enables Enterprise-Wide Fraud Detection in Banking

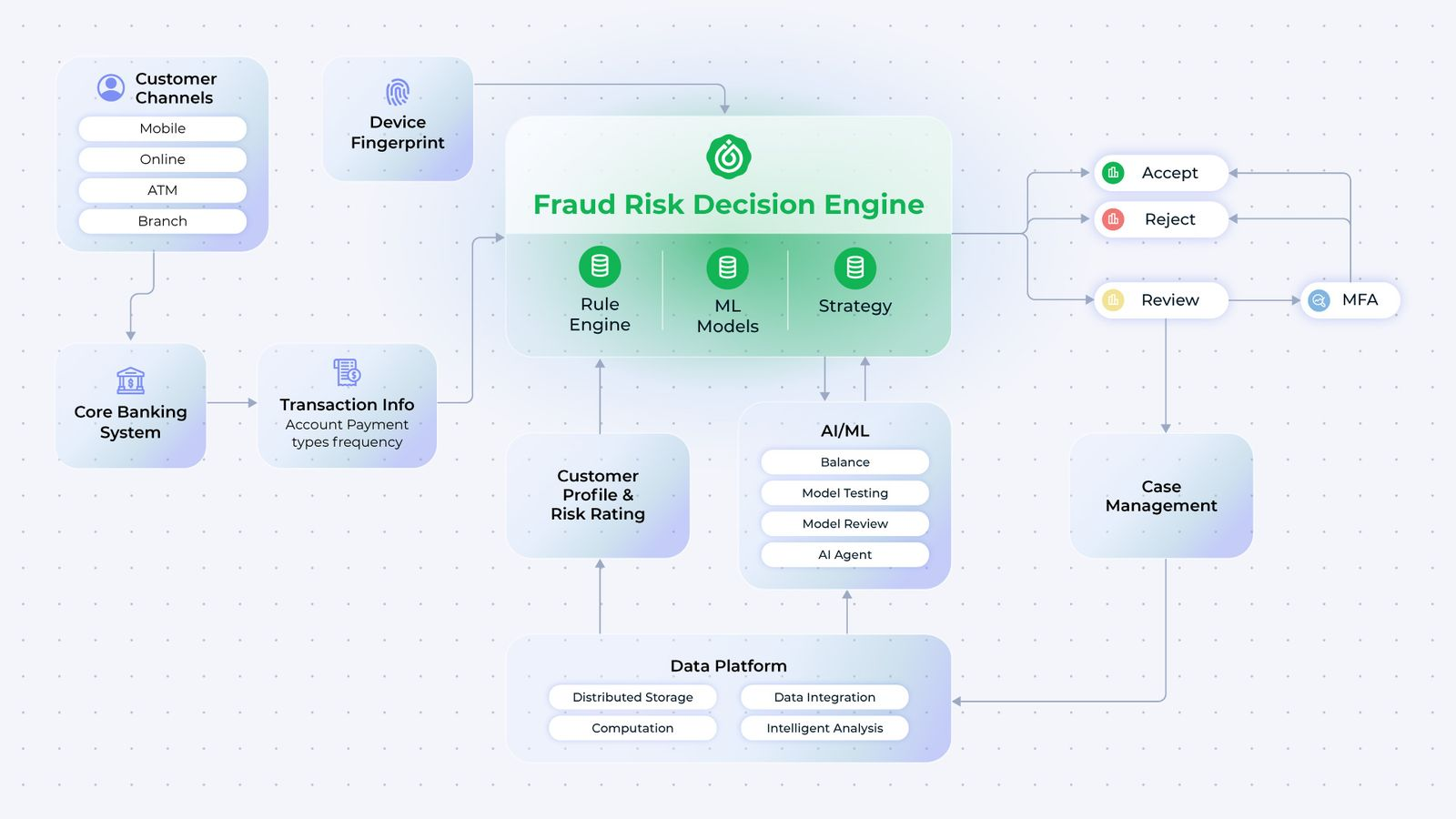

TrustDecision enables the shift from fraud strategy to execution through a tightly integrated architecture built on ARCHER® Risk Decisioning OS and ARGUS® Fraud Management Platform, designed specifically for banks and fintechs operating at scale.

ARCHER® Risk Decisioning OS functions as the scenario-less decision intelligence operating system. It orchestrates data, rules, models, and workflows across fraud, credit risk, and compliance use cases—ensuring strategies are defined, governed, and applied consistently across onboarding, lending, and transaction monitoring.

ARGUS® Fraud Management Platform operates as the anti-fraud system within this architecture. It applies centrally defined anti-fraud strategies to events and transactions by monitoring activity across channels, evaluating risk from both real time channels and off-line data sources, and supporting investigation and response workflows powered by AI-driven models.

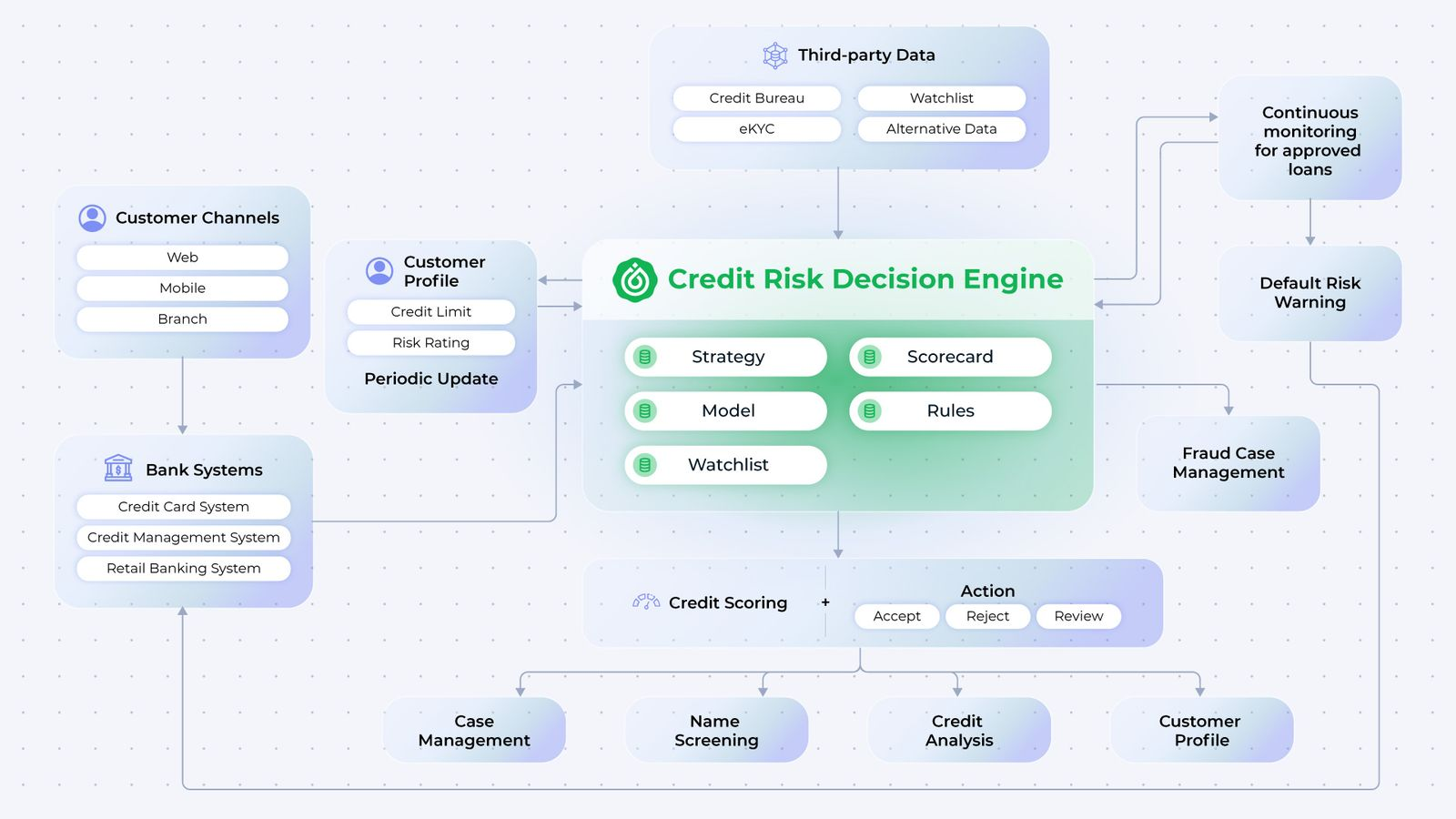

Extending Risk Decisioning into Credit Management with PISTIS®

Beyond fraud prevention, TrustDecision extends its decision intelligence architecture into credit operations through PISTIS® Credit Management Platform. PISTIS® enables banks to manage credit risk across the full credit lifecycle—from origination and underwriting to limit management, monitoring, and collections.

By leveraging the same decisioning principles as ARCHER®, PISTIS® allows credit strategies to be governed centrally and executed consistently using shared data, models, and policies. This ensures tighter alignment between fraud risk and credit risk decisioning, helping banks improve portfolio performance, reduce losses, and maintain regulatory compliance at scale.

Together, ARCHER® and ARGUS® enable banks to:

- Detect and respond to fraud in real time across channels

- Reduce false positives while maintaining low customer friction

- Apply fraud strategies consistently across the customer lifecycle

- Scale fraud prevention without increasing operational complexity

Core TrustDecision capabilities include:

- ARGUS® Fraud Management Platform – Enterprise fraud management and real-time transaction monitoring

- Application Fraud Detection – Prevention of identity, document, and synthetic fraud during digital onboarding

- Identity Verification (eKYC) – Biometric verification, liveness detection, and AML/KYC screening

- Promotion Abuse Prevention – Protects digital banks from incentive abuse and account farming

- Credit Risk Decisioning – AI-powered credit assessment and automated credit decisions

TrustDecision enables banks to operationalise fraud prevention consistently and at scale—strengthening enterprise-wide risk control across the banking lifecycle.

Conclusion: Building Resilient, AI-Driven Fraud Detection in Banking

Banking fraud continues to evolve in scale, sophistication, and speed. As fraudsters exploit digital channels, human vulnerabilities, and fragmented systems, traditional, siloed controls are no longer sufficient to protect modern banking environments.

Fraud detection in banking using AI and machine learning moves beyond reactive, rule-based approaches by:

- Detecting fraud in real time across transactions, accounts, and channels

- Reducing false positives while maintaining low customer friction

- Applying fraud controls consistently across the customer lifecycle

- Adapting rapidly to new and emerging fraud patterns

However, the true advantage comes from how these capabilities are operationalised. By unifying fraud strategy and execution within a single decision intelligence architecture, banks gain the visibility, control, and scalability required to manage fraud effectively across onboarding, lending, and ongoing account activity.

Ready to stress-test your fraud defenses?

Request a demo today or Speak with TrustDecision’s fraud prevention specialists to see how ARGUS® Fraud Management Platform and PISTIS® Credit Management Platform enable real-time, AI-driven fraud detection and prevention across the banking lifecycle.

FAQs:

What is fraud detection in banking?

Fraud detection in banking is the process of identifying and preventing unauthorised or deceptive financial activity across digital onboarding, transactions, and ongoing account behaviour. Modern systems combine rules, analytics, and AI models to assess risk in real time while minimising customer friction.

How does AI improve fraud detection in banking?

AI enables banks to analyse large volumes of transactional and behavioural data in real time, detect complex fraud patterns, reduce false positives, and adapt quickly to new fraud tactics.

By 2026, 60% of new bank fraud detection deployments will use customer-centric, AI-driven platforms, replacing siloed rule-based systems (Gartner, Buyer’s Guide for Fraud Detection Technology in Banking, 2023).

What types of fraud can AI-based systems detect?

AI-based fraud detection can identify:

- Card and payment fraud

- Account takeover (ATO)

- Application and document fraud

- Synthetic identity fraud

- P2P payment scams

- Loan fraud and suspicious transaction patterns

How does real-time monitoring improve fraud detection outcomes?

Real-time monitoring analyses transactions and account activity within milliseconds using multiple risk signals. This allows banks to block or step up verification for high-risk activity instantly, while allowing legitimate transactions to proceed with minimal disruption.

How does enterprise fraud management improve efficiency?

Enterprise fraud management unifies fraud detection, investigation, and response across channels and products. By applying consistent fraud strategies across the customer lifecycle, banks reduce manual reviews, lower false positives, and improve operational efficiency at scale.

How does TrustDecision support real-time fraud detection?

TrustDecision enables real-time fraud detection by orchestrating fraud decisions across identity verification, application fraud detection, transaction monitoring, and credit risk workflows—ensuring consistent risk decisions across channels.

What is TrustDecision’s ARCHER® Risk Decisioning OS?

ARCHER® Risk Decisioning OS is TrustDecision’s enterprise decision intelligence platform. It orchestrates data, rules, and AI models in real time to apply fraud strategies consistently across onboarding, lending, transactions, and account activity.

What is the ARGUS® Fraud Management Platform?

ARGUS® Fraud Management Platform is TrustDecision’s enterprise fraud execution layer. It monitors live activity, evaluates risk in real time, and supports alerts and investigations—turning centrally defined fraud strategies into operational action.

What is TrustDecision’s PISTIS® Credit Management Platform?

PISTIS® Credit Management Platform is TrustDecision’s credit risk management platform that supports the full credit lifecycle—from origination and underwriting to monitoring and collections. It enables banks to govern credit strategies centrally using shared data, models, and policies, improving decision quality, reducing losses, and supporting regulatory compliance at scale.

Can TrustDecision integrate with existing banking systems?

Yes. TrustDecision integrates with core banking systems, digital channels, payment rails, and third-party data sources via APIs and a modular architecture, allowing banks to enhance fraud prevention without replacing existing infrastructure. Speak with TrustDecision’s fraud specialists today to assess how this integration can support your fraud prevention strategy.