Running an e-commerce business comes with its fair share of challenges, but few are as frustrating and damaging as fraud. Picture this: you’ve spent all the marketing budget to advertise your brand and products, attracted a steady flow of customers, and suddenly you’re hit with a wave of spammy registration, promotion abuse, chargebacks and all sorts of anomalies. It’s a common scenario that businesses face, often underestimated the complexity and importance of fraud prevention.

The stakes are high, with global e-commerce fraud losses projected to exceed $48 billion globally in 2023. Whether you’re a startup experiencing increased transaction volumes or an established enterprise expanding internationally, understanding when and how to upgrade fraud management approach is key. Most e-commerce businesses will leverage on fraud prevention offered by payment gateways they’re engaging with. Here we break down the differences between that and a third-party solution provider — pros and cons comparison, and factors to consider.

Payment Gateway Fraud Prevention

Most established payment gateways offer built-in fraud prevention tools that focus on transaction phase of the customer journey. These tools are designed to detect and block common fraudulent activities during transaction, providing a layer of security integrated directly into the payment processing flow. it is convenient and cost-effective solution as it requires minimal setup and maintenance, in some cases included at no additional cost.

The challenge kicks in when an e-commerce business scales up, where operation become more complex and potentially let their guard down in risk management. These are exactly the type of online stores fraudsters love targeting, especially products with high resell values. A broad spectrum of threats out of the payment journey including fake registrations, scalping, money laundering, inventory hoarding, and other sophisticated fraud schemes are difficult to address by payment gateways.

For merchants serving cross-borders across different regions and necessitating multiple payment channels. Each channel governed by its own set of risk control protocols complicates the task of maintaining uniform risk management standards across the store. This fragmentation can lead to inconsistencies in customer experience and gaps in security measures.

Third-Party Fraud Solution Provider

Not all, but some fraud prevention vendors offer platforms that cover wider fraud journey, from user onboarding to post-transaction monitoring. A comprehensive coverage of fraud detection system should look like this:

- User onboarding: The process begins with scrutinising new user registration and logins, deploying verification techniques such as behavioural analytics and device fingerprinting to identify suspicious activity from the outset and differentiate human / bot registration. This early detection and considering broader user behaviour patterns allow for more accurate assessment during the transaction phase.

- Pre-Transaction monitoring: Before it reaches to the payment stage, there’re signs to identify through browsing behaviour, frequency, timing, historical data and patterns among/across the user segment.

- Transaction approval: At the transaction stage, real-time risk assessment is the key and this can be achieved by machine learning models that consider a wide array of data points to ensure that legitimate transactions are processed while fraudulent ones are flagged or blocks immediately.

- Post-transaction analysis: This part is crucial for identifying fraud that may not be immediately evident during the initial transaction. Services such as chargeback alert allows merchant to resolve the dispute with customers before it escalates to the banks and result in chargeback.

- Promotion or referral program: During promotional campaigns, the key is to get the most ROI out of your bucks spent. A good solution provider should detect abuse such as using multiple accounts to claim discounts, exploiting referral programs, or redeeming multiple vouchers.

Given that fraud risk management is the core business of these third-party solution providers, they don’t compromise on technology. Also, merchant can leverage on the extensive data sources from their global network of database to detect fraud easier and faster.

We can’t say it for all but we can say it for ourselves. At TrustDecision, we found out that 10% of the high-risk transactions are linked to devices with fraud-related applications. That’s why, we have a dedicated team to constantly improvise our device fingerprinting technology while keeping it compliance to all application stores.

With an extensive experience in black market research and anti-fraud expertise, we provide customised strategies and models tailored to specific industry needs. We put high focus on continuous improvement of strategic models, based on the evolving impact of risks, ensures an effective joint defense mechanism across different payment channels.

TrustDecision incorporate our in-house datasets and collaboratively broaden the range of data sources from other channels as well. This extensive data collection enhances our capability to conduct a more nuance risk assessment, offering a more complete perspective than typically available through internal risk control.

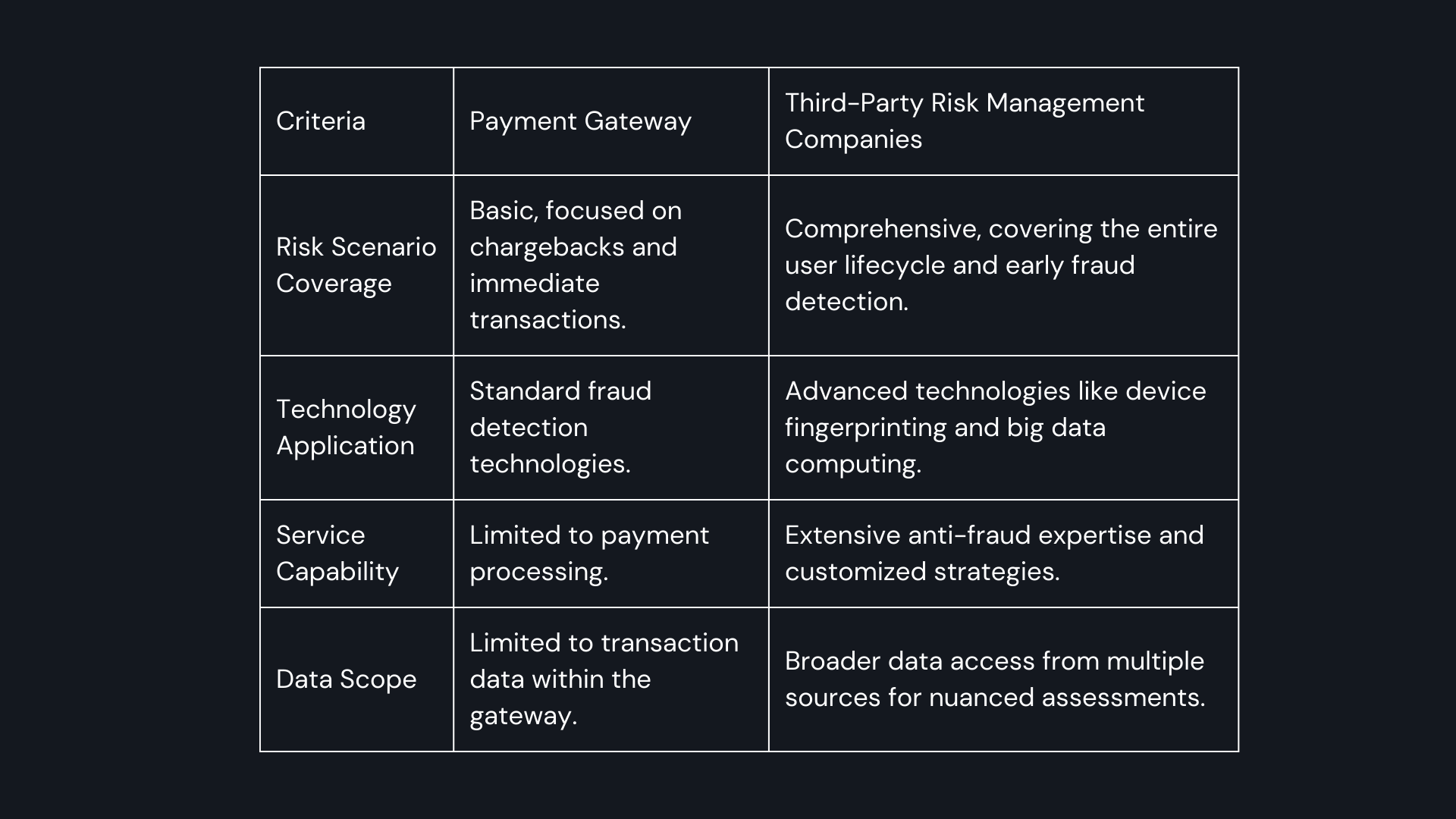

Here’s an overview of comparison:

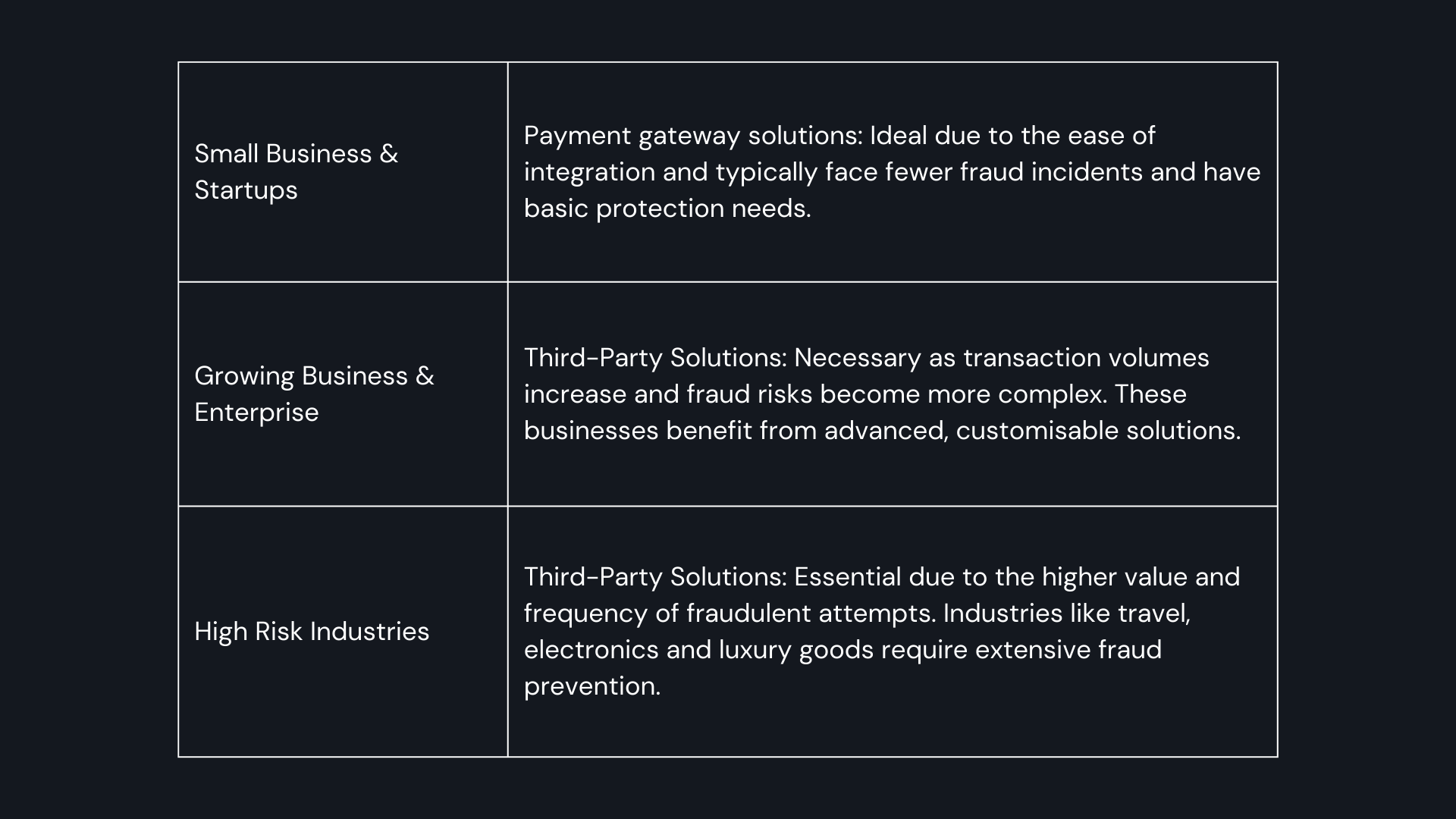

Factors to Consider the Right Fraud Management for Your Business

Steps to Choose the Right Solution

- Assess your needs: Conduct a detailed assessment of your current and future fraud risks

- Analyse transaction data: Examine past transactions patterns of fraudulent activities and its segment by various criteria like geographical location, payment method, transaction size, and customer type.

- Evaluate current fraud incident: Document and analyse all past fraud incident, determine the root cause and understand vulnerabilities in your current systems

- Forecast future risks: Consider how business growth and expansion, especially into new markets might introduce new fraud risks and the company’s risk appetite.

- Evaluate options: Compare the feature, cost and capabilities of payment gateways and third-party solutions

- Trial and feedback: Pilot a trial with a few alternatives and see what works best for your business

- Continuous monitoring and improvement: Regular review of your current fraud prevention strategies and keep up to date on the latest technologies available for optimisation — be it capability, cost or efficiency wise.

In a Nutshell

Selecting the right fraud management strategy is critical for protecting your e-commerce business. While payment gateway solution offer convenience, third-party solution providers can deliver advanced and customisable protection necessary for growing and high-risk businesses. Evaluate your needs, understand your risks, and choose a solution that balances security, cost, and customer experience.