Hello from the Other Side (It’s Not Adele This Time)

Telecom fraud leaves banks at the end of the damage chain. Discover how real-time intelligence and closed-loop frameworks help stop fraud before it spreads.

Get comprehensive guide about email, phone number and IP profiling – its usage to prevent fraud at each stage of the user journey, detailed data you can get and how you can start a free trial.

Unknown numbers? Straight to voicemail. Even friends? Maybe later. It’s not just social anxiety or convenience. It’s survival.

Every ring now carries a shadow. We’ve seen too many stories about fake bank officers, “parcel delivery” scams, calls that start with curiosity and end with drained savings. And we’ve learned to pause before we say “hello” — it’s a post-trauma self-defense of telecom fraud.

The Fraud Problem Banks Can’t Hang Up On

For every individual who hangs up on a scammer, there’s another who gets trapped: the social engineering calls that lure out personal details, the SIM swaps that take over phone numbers, the phishing links that steal login data, and somewhere, a facepalm moment echoes: “I should have known better.”

Here’s what you should know better:

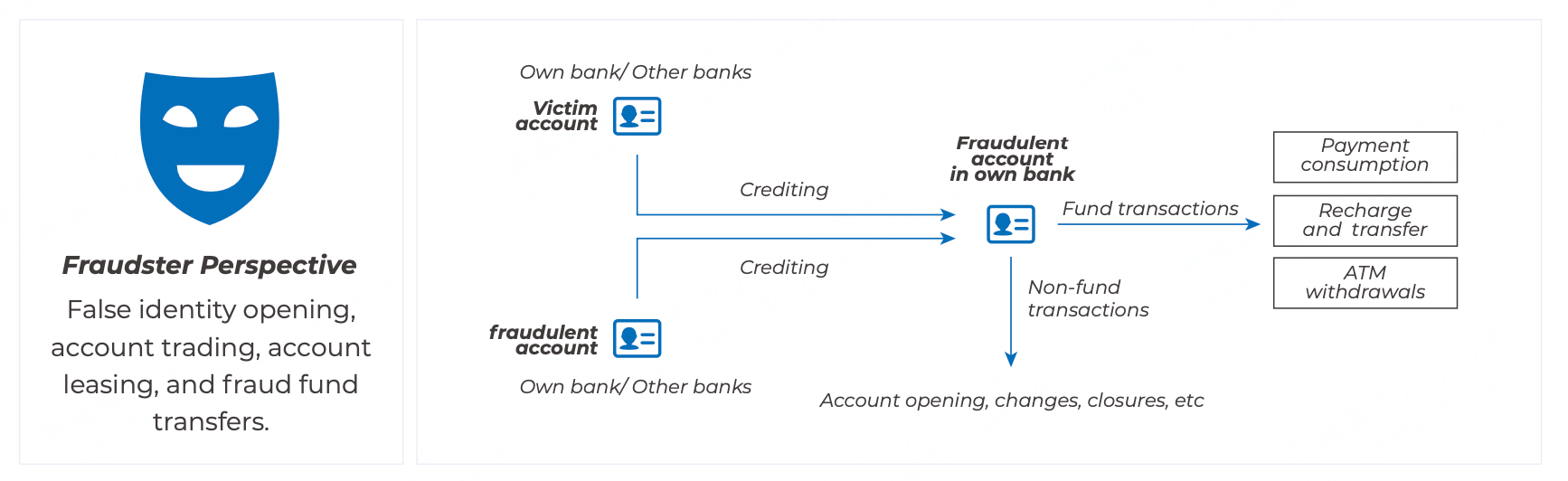

The victim’s money lands in the fraudster’s account: sometimes in the same bank, sometimes elsewhere. From there, it doesn’t stay still. Within seconds, the balance is split and rerouted across a web of mule accounts (often opened with fake identity, bought, or rented), third-party wallets, and cross-bank transfers.

Each hop blurs the trail a little more, until what started as one transfer becomes a maze of transactions: payments, top-ups, withdrawals, even crypto exchanges. By the time someone realizes it’s fraud, the funds have already scattered beyond recovery.

Banks Still Struggle to Capture Fraud Network, Why?

By the time the funds scatter, it’s not just a victim’s problem but bank’s.Every transaction, every dormant account, every false positive becomes a number in the next regulatory ranking.

Across Southeast Asia, banks face growing pressure from both regulators and law enforcement authorities to report mule accounts and scammed victims . But the reality behind those targets is far from simple.

High pressure, low precision

Public security agencies demand faster and stronger reductions in compromised accounts. But for most banks, the identification rate is low and investigation cost high.

Labelled samples are scarce and expensive to obtain, making it hard to train accurate models. The result? Too many false positives, overloaded manual reviews, and spiraling operational costs — all while large-scale fraud still slips through.

Organized fraud rings evade conventional defenses

These aren’t lone scammers anymore. Professional, well-coordinated syndicates manipulate networks of fake or rented accounts to bypass detection. Their activities blend seamlessly into massive volumes of normal behavior, making it nearly impossible for static rule or model systems to tell signal from noise.

Delayed detection, weak real-time control

By the time a suspicious account is confirmed, it’s often too late. Many banks still lack cross-channel, decision-making systems that can intercept risk before or during the transaction. Those relying on simple rule triggers face the opposite problem: too many alerts, too little accuracy. The result is both regulatory exposure and customer friction.

Rapid model decay, short-lived strategies

Telecom fraud evolves faster than most models can keep up. Every week brings new tactics — from social engineering scripts to cross-border payment routes. Single-model defenses decay quickly, forcing constant retraining and manual tuning. Without adaptive optimization, even good models lose effectiveness within months.

A Framework to Relieve the Pressure

There’s no single silver bullet to stop telecom fraud, but there is a system that works.

Combatting telecom fraud needs a framework that combines structured data, domain expert strategy, risk modeling and graph intelligence to spot fraudulent fund transfer while staying compliant and cost-efficient.

Detect Before Damage Happens

It starts before a single transaction takes place. By enhancing account-opening supervision and running predictive models on new or sleeping accounts, banks can spot fake, leased, or suspicious profiles early. These models look beyond static identity checks — analyzing behavior, device signals, and connection patterns to flag high-risk accounts before they become conduits for fraud.

Real-Time Monitoring and Interception

Once funds start moving, speed matters. Real-time transaction monitoring models analyze every credit and debit flow across channels, identifying patterns typical of telecom fraud, such as rapid fund splitting, cross-institution transfers, or suspicious top-ups.

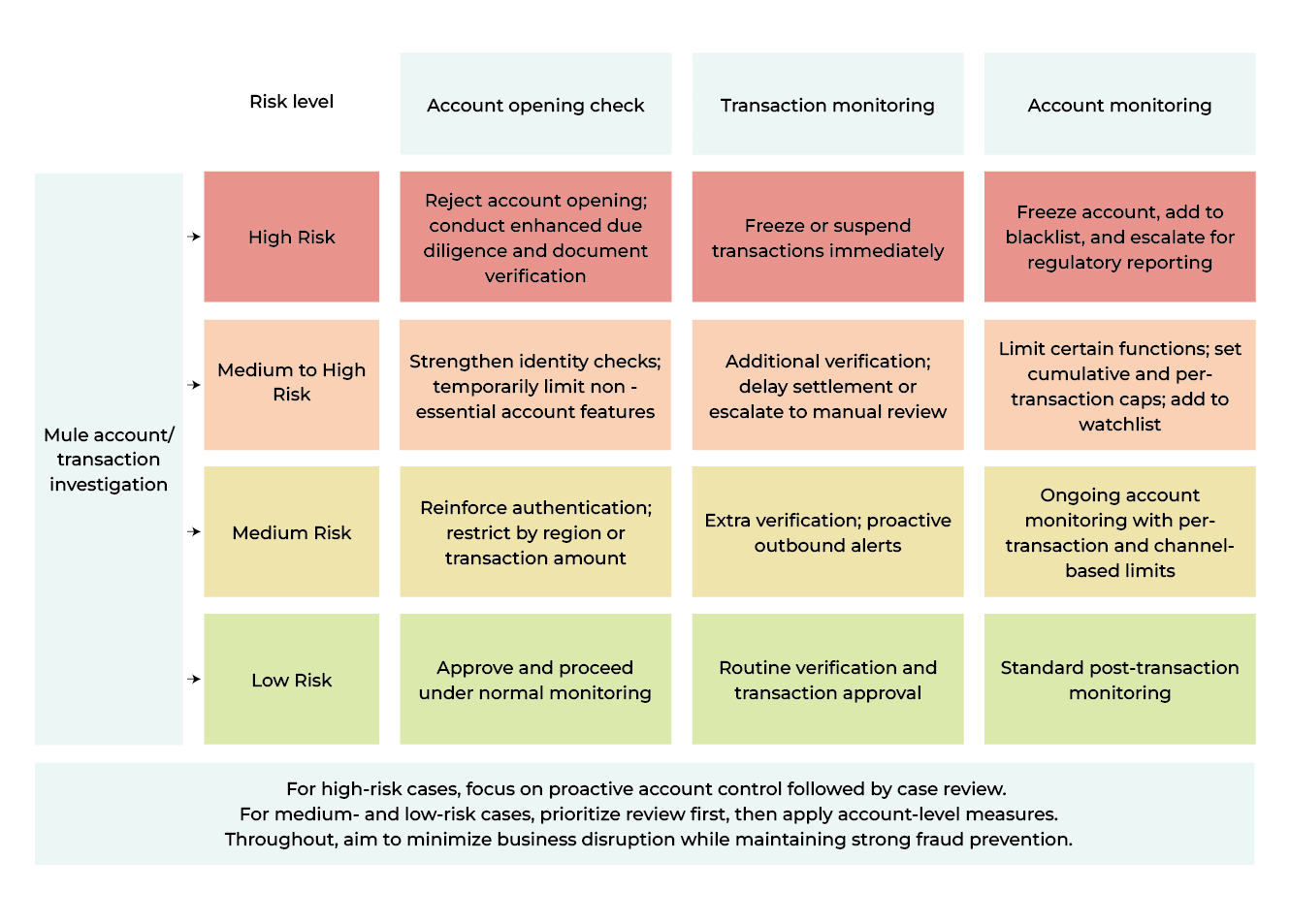

The system enforces granular, dynamic controls based on risk levels:

High-risk → temporary holds, enhanced authentication, or transaction blocks

Medium-risk → delayed settlement or manual review

Low-risk → standard processing with continuous monitoring

Continuous Strategy Optimization Loop

When fraud has already occurred, intelligence takes over. The post-event mining and graph analysis layer connects related accounts through transaction links, shared devices, or overlapping credentials, surfacing hidden fraud rings and dormant mule networks.

These findings feed back into the model library, enabling continuous optimization and more accurate pressure-drop ranking in future cycles.

Evolving with the Threat

Finally, the framework isn’t static. Models are retrained with new data; strategies refined with expert consultation.

Each phase (before, during and after fraud case) reinforces the next, forming a closed-loop system that balances risk management operational efficiency, and business continuity.

Listen To the Signals

Every call we don’t pick up says something about the world we live in — cautious, alert, a little scarred. But maybe that’s also how resilience begins: by learning to listen carefully before we answer.

For banks, listening means decoding signals before they turn into losses. Listen to the signals and answer with the right decision. You need intelligence that reacts in milliseconds, systems that evolve with every new tactic, and decisions that stay consistent under pressure.

Subscribe to our newsletter to get real insights, fraud analysis, innovative technology updates and latest industry trends

.jpg)