The Bad Apples of Loan Brokers: How They Falsify Borrowers and Defraud Lenders

What if some of your own credit applicants are working hand in hand with fraudsters? Discover how professional loan brokers operate to cheat your lending system, and how financial institutions can break their schemes.

Get comprehensive guide about email, phone number and IP profiling – its usage to prevent fraud at each stage of the user journey, detailed data you can get and how you can start a free trial.

The file lands on the underwriter’s desk – six months of financial statements, with each month performing better than the last. Credit score in the highest bracket. Income high enough to qualify for a premium limit. Even the debt-to-income ratio looks enviable.

Everything screams a ideal borrower. The system not only approves the application, it offers a credit line larger than the applicant requested. But somewhere outside the bank’s walls, a different calculation has already been made.

The borrower’s spotless record wasn’t built on discipline. Their profiles and credit histories are carefully packaged by loan brokers who know exactly how to craft a profile for maximum approval. In return, these broker claim a hefty cut of the disbursed loan as their commissions.

When the first repayment is missed, the illusion shattered. The bank is left staring at a massive default, the borrower is buried under a debt they can’t repay, and the loan brokers walk away untouched, pockets lined with commission, bearing neither cost nor consequence.

Around the world, a silent epidemic is hitting banks – fraud engineered at scale. And it's getting smarter, faster and harder to detect.

In Makassar, Indonesia, state bank employees and brokers colluded to fabricate applications for over a hundred ineligible borrowers – skimming up to 10% "fees". In Vietnam’s Lao Cai province, fraudsters preyed on financially inexperienced highland residents, tricking them into signing false contracts so loan funds could be siphoned off.

In the Philippines, the notorious “ghost borrower” housing loan scandal exposed developers and brokers used dummy applicants to drain millions of government housing funds before defaulting.

This not only happens in the emerging markets. In the United States’ subprime mortgage crisis also fits the pattern: massive issuance of home loans to unqualified borrowers, later repackaged and sold, leaving banks, investors, and borrowers devastated. In each instance, intermediaries profit immediately, walking away with commissions, while borrowers bear the legal liability and lenders absorb the financial hit.

How the Scheme Works

They don’t all play the same game, they operate like financial engineers. Beneath the case is a toolbox of schemes, each tailored to the borrower's profile, each designed to make the loan approval process look legitimate and risk-free.

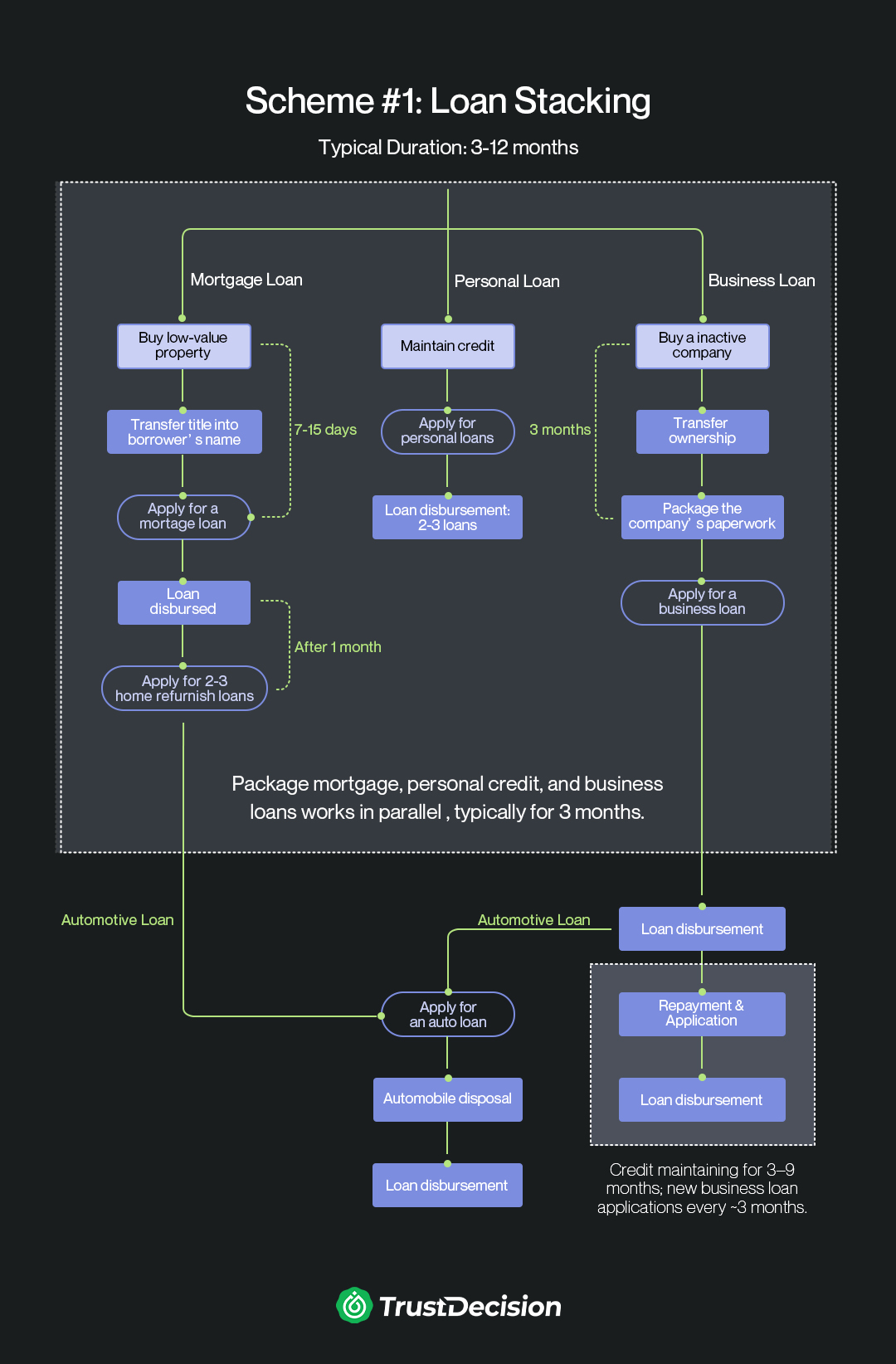

Scheme 1: Loan Stacking

A high-speed, high-yield tactic where multiple loans are piled onto a single borrower. Housing loans, car loans, credit loans, and even business loans — all applied within a short window, to maximize the total borrowed amount before the system catches up.

The Three Steps

Background PackagingFraud brokers manufacture credibility. To make the borrowers "eligible" for these loans, they help borrowers to purchase companies or real estate in poor condition. This allows them to pose as a "business owners" or "property investors", who are typically qualify for higher credit limits.

Loan Stacking. After dressing the profile, applications are submitted across multiple channels, like mortgage, auto loans, personal credit, and business loans – often within days or weeks. Each loan is handled by the different intermediary, ensuring the speed of approvals.

Payout and skimming.As soon as the funds land, the brokers take 10–30% in commissions immediately. The borrower typically walks away with 40–60% of the total, but carries 100% of the liability. When the repayment stall (which they almost always do), the bank absorbs the loss while the victim suffers in debt.

This type of scheme usually target those who are aged 25 to 55 with a clean credit history, lower education, able to follow instructions, desperate for cash or quick profit, and often unaware of the legal risk, trusting brokers’ promises of easy approval.

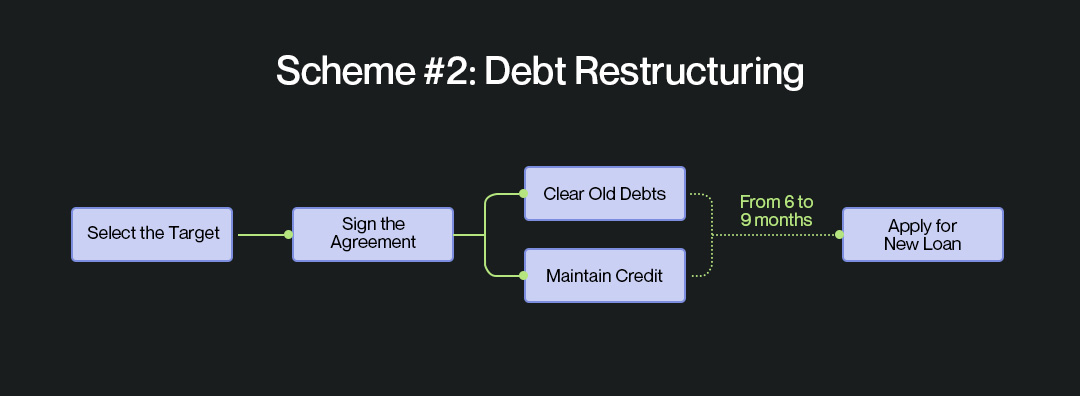

Scheme 2: Debt Restructuring

Instead of rushing to stack loans, this scam plays the long game. The fraud ring “helps” the borrower pay off old debts and polish their credit record, making them look like a low-risk, high-credit borrower. Once the credit report is clean, they quickly apply for high-value loans, often times through public housing fund loans and large bank credit loans.

The Three Steps

Debt clearance & credit grooming. The broker injects funds to pay off overdue accounts, remove negative marks, and improve the credit score.

Loan application blitz. Within a short period of time, they applied for multiple new loans. For example, in China, the loan typically ramps from RMB 300,000 to 3 million (USD 40,000–420,000), usually from banks and public housing loan programs.

Payout & commission. After loan disbursement, the broker takes a 20–30% cut immediately, and the borrower gets the rest but remains fully liable for repayment.

This type of scheme typically targets adults with stable and reputable jobs such as government employees, doctors, teachers, or staff at well-known companies; often already heavily indebted but unable to get new loans directly. They’re in urgent need of a large sum to relieve financial stress, and trust brokers who promise a quick fix and higher loan approval.

The Counterattack

It’s typical to see that these fraudsters playing the long game: applying using engineered borrower profiles, making a few on-time repayments to build trust, pushing for higher limits, and then cashing out large sums before defaulting.

To combat this, lenders must look beyond surface-level documents and deploy defense strategy that spans across the entire lending cycle. Drawing on years of research and field experience, TrustDecision recommends a three-stage defense that covers pre-loan, mid-loan, and post-loan controls.

Before Lending: Break the Illusion Early

The first line of defense is to strip away the mask before the loan is ever approved. Go beyond surface checks and verify the borrower’s identity, employment, assets, and income through independent channels, not just the documents they hand over.

Cross-check company registrations, ownership structures, and past credit behavior. A spotless record that appeared only in the last few months should raise questions, not confidence. By connecting scattered data points into a complete borrower profile, lenders can see whether they’re dealing with a genuine applicant or a carefully staged performance.

During Lending: Control the Gate

Once an application makes it past initial screening, the next challenge is precision at credit underwriting. Fraudsters thrive on inflated amounts and vague terms. Don't just rely on borrower-declared income or documents they provide. Independently verify their salary, business revenue, operating cashflows, or other repayment sources. Request for concrete evidence for the loan’s purpose — signed contracts, supplier invoices, or purchase orders — and match disbursement schedules to genuine business needs.

Lenders should practice dynamic risk-based pricing, adjust loan terms and collateral requirements based on borrower's actual risk profiles. This keeps capital from being front-loaded and misused, while still moving legitimate loans forward.

After Lending: Monitor Like a Crime Scene

The real test begins after disbursement. Funds should be tracked in real time to ensure they follow the intended path, with alerts triggered by unusual transfers, sudden cash withdrawals, or cycling through unrelated accounts. Combine transaction monitoring with predictive risk analytics models that watch for early warning signs: delayed payments, unexpected credit changes, or shifts in the borrower’s industry. When the first cracks appear, act fast — whether that’s an early intervention, repayment restructuring, or a freeze on further disbursements.

In a Nutshell

From stacked loan schemes to staged credit grooming, the patterns are there for lenders willing to look beyond the surface.

Every falsified profile, every staged repayment, and every engineered default chips away at lenders’ trust, drains capital, and leaves borrowers trapped in debt. The bad apples will always look for new ways to exploit the gaps, but lenders are not powerless.

With stronger verification, data-driven monitoring, and a proactive defense strategy, financial institutions can close the cracks these schemes rely on. The cost of inaction is steep, but the reward of vigilance is clear: protecting both borrowers and the financial system from being engineered into collapse.

Subscribe to our newsletter to get real insights, fraud analysis, innovative technology updates and latest industry trends

.jpg)

-2.png)